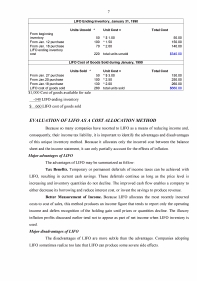

Darbas anglų kalba. Inventoriaus vertinimas. Introduction. Nature of inventory. Classes of inventory. Inventory valuation methods. FIFO method. Weighted average method. LIFO method. Evaluation of LIFO as a cost allocation method. Major advantages of LIFO. Major disadvantages of LIFO. Specific identification method. FIFO. Weighted average. LIFO. Specific identification. Comparing inventory cost methods. Examples. Characteristics of each method. Other cost methods. Cost of latest purchases. Standard costs. Direct costing. The retail method. Conclusion.

82.54 KB

82.54 KB